What is euphemistically called “fractional-reserve banking” is obvious fraud, and obvious crime. By its very definition; it transforms the banking sector of an economy into a leveraged Ponzi-scheme, and as with all Ponzi-schemes, there is no possible “happy ending” here.

Mathematically-based principles are often illustrated best through use of an extreme, numerical example. We have no need to construct any hypothetical extremes, however, when we already have real-life insanity, in our current monetary/regulatory framework.

-

The Cabal Fire Worm Cometh May 2016 vs Physical Silver & Gold

-

Globalist’s Federal Reserve ~ The Dollar’s Homecoming: Gold & Silver Shorting By Bullion Banks To Bolster Image Of Fiat U.S. Dollar

![Central Bank of Iraq finalises agreement with Zaha Hadid Architects to design new office headquarters in central Baghdad The Central Bank of Iraq on February 2 signed an agreement to begin the process of building new headquarters on the shores of the Tigris River in Baghdad. "The new building shall be a symbol of the [central] bank's role in the economic development of Iraq and a reflection of the determination to rebuild the country,"](https://rasica.files.wordpress.com/2015/11/screen_shot_2013-11-14_at_11-18-36_am-jpg.png?w=547)

Central Bank of Iraq finalises agreement with Zaha Hadid Architects to design new office headquarters in central Baghdad The Central Bank of Iraq on February 2 signed an agreement to begin the process of building new headquarters on the shores of the Tigris River in Baghdad. “The new building shall be a symbol of the [central] bank’s role in the economic development of Iraq and a reflection of the determination to rebuild the country.” The £630 million building will be built on a 20 hectare site in West Baghdad, which was originally used by Saddam Hussein to partially construct a super mosque.

J.P. Morgan was ‘granted’ the rights to, effectively, set up the Central Bank of Iraq in Dec. 2003:

-

J.P. Morgan Chase was chosen by the Coalition Provisional Authority [CPA] to ‘set up’ the NEW Central Bank of Iraq [specifically, the Trade Bank of Iraq ].

-

Take note how this TRADE BANK only became operational in December of 2003:

-

Trade Finance. The Trade Bank of Iraq (TBI) was established in July 2003 to facilitate trade of goods and services to and from Iraq by providing irrevocable letters of credit.

-

The TBI officially became fully operational in December 2003 and has a services contract with a multi-international banking consortium led by JP Morgan Chase.

-

Since opening in December, the Trade Bank of Iraq has issued or has pending 183 letters of credit, totaling $708.9 million in imports from thirty-one countries.

-

Letters of credit have been issued on behalf of Iraqi Ministries as well as several state-owned enterprises.

-

In that capacity, Morgan was charged with developing the framework of collateralizing movable and immovable property for the nation of Iraq.

-

The fact is that one of the largest derivatives facilitators [aka paper promissory notes aka fractional digital banking scheme] in the world is one of the principal architects of the Trade Bank of Iraq,

-

plus it is also well-known that J.P. Morgan has a direct connection to the Rothschild banking dynasty ~~ a trend that is to be seen in virtually every central and major bank in existence across the planet.

Activist Post

Iraq’s IQD 2016: Presently not released from “tight monetary controls” Iraq is under siege by the Cabal’s IMF preventing International Exchange.

-

General Flynn & Hillary Clinton Confirms U.S. Israeli ISIS: Splitting Iraq & Syria For Israel.

-

Iraq Must Stay Divided & Isolated From Its Regional Environment: Israeli Minister of Internal Security Shin Bet aka; ISIS.

-

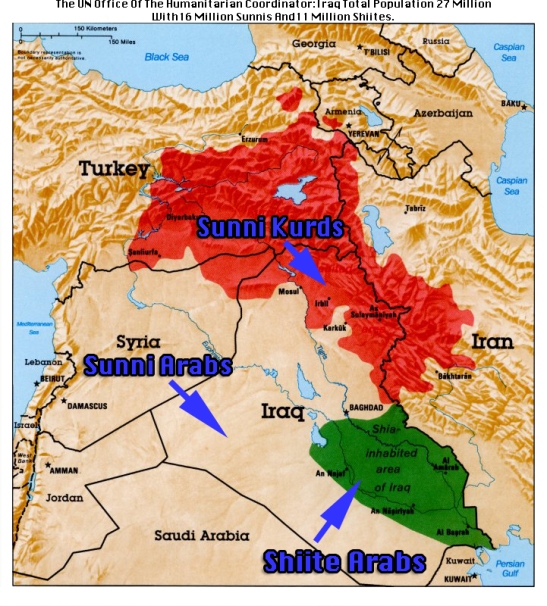

U.N. Office Humanitarian Coordinator For Iraq: Population Statistics Show Iraq’s Sunnis Are In Clear Majority At 16 Million Sunnis & 11 Million Shiites.

Here it is important to note that in order to conceal the fraud, crime, and insanity of our present system to the greatest degree possible, the bankers hide their dirty deeds within their own convoluted jargon. Thus presenting “fractional-reserve banking” to readers requires some brief investment of time in definition of terms, starting with this term, itself.

Fractional-reserve banking evolved literally based upon the temptation of all bankers to perpetrate fraud. Empirically it has always been observed, down through the centuries, that under normal circumstances, only a tiny percentage of depositors will come to claim their cash/wealth at any one time.

Thus the temptation is for bankers to “lend” more funds than they actually possess, i.e. they are “lending” what does not even exist: “fractional-reserve banking” ~ the ultimate euphemism of banking and fraud.

Indebting: To bring into debt; to place under obligation;

~ chiefly used in the participle indebted. [1913 Webster]

Iraq’s New Parliamentary Building ~~ She goes up ~ a vast new $1-billion parliamentary complex in Baghdad. The well-known London-based, Iraqi-born architect Zaha Hadid has been tapped to design a 2.7-million-square-foot building on the 49-acre site.

Iraq’s New Parliamentary Building ~~ She goes up ~ a vast new $1-billion parliamentary complex in Baghdad. The well-known London-based, Iraqi-born architect Zaha Hadid has been tapped to design a 2.7-million-square-foot building on the 49-acre site.

Up until the false flag attacks by Israel, and Israel Firsters in the US government, on the WTC in New York on 9-11-2001, there were 7 countries left in the world who had not buckled to pressure, who had not resigned themselves to slavery under the Rothschild fractional reserve banking system. Those countries were Afghanistan, Cuba, Iran, Iraq, Libya, North Korea and Sudan. But Now There Are More!

It goes without saying that anyone or any entity which endeavours to “lend” something which does not exist is perpetrating fraud.

Iraq ChamChamal Prison $29 Million. Wasting No Time ~ It Was Completed In 2009.

‘STAGNATION’

A prolonged period of little or no growth in the economy. Economic growth of less than 2 to 3% annually is considered stagnation. Periods of stagnation are also marked by high unemployment and involuntary part-time employment. Stagnation can also occur on a smaller scale in specific industries or companies or with wages.

In late 2012, supporters said the Federal Reserve’s third round of quantitative easing [printing currency either digitally or physically] was necessary to help the United States avoid economic stagnation.

The central bank’s proposed asset purchases of mortgage-backed debt were expected to foster economic growth, bolster the housing market and improve employment prospects.

The Fed also kept interest rates low as part of its plan to prevent stagnation.

Investopedia

IT BECAME WORSE BY 2015

But before examining this inherent fraud more closely, it is important to back-up, and look at the Law. Note that even when banks “lend” the money which they actually do hold on deposit (as trustees for the depositors) that this is already wholly/totally illegal.

Gates Rothschild NWO

It is the crime known as “conversion”.

France ~ David de Rothschild

France Indicts David de Rothschild For Bank Fraud: Manhunt On As Judge Orders Police To Track Down Rothschild.

“We’re Running A F—ing Casino”: Politician “X” Tells All In Manifesto!

Criminal conversion:

A person who knowingly or intentionally exerts unauthorized control over property of another person commits criminal conversion.

When your bank lends-out money you deposited, which it claims to be “holding” for you as trustee, does it seek your prior authorization before lending-out your property and thus putting it at risk? Of course not. The banks get around the naked criminality of their lending operations through general authorization.

In the small-print of any/all bank deposit contracts is a clause whereby the depositor “authorizes” the bank to lend-out their property to Third Parties.

We therefore start with the basic fact, that “banking” as we know it (bankers taking deposits, and then lending those deposits) is literally institutionalized crime.

But “Fractional-reserve banking” goes far beyond this original level of criminality.

Not only are banks allowed to lend what they don’t own, they are allowed to lend what they don’t even possess – and by many multiples.

“Banking” is institutionalized crime. “Fractional-reserve banking” piles-on a systemic and enormous element of fraud: “lending” what does not even exist. But this isn’t even the most-shocking aspect of fractional-reserve fraud.

Rothschild Billionaire Mahafarid Amir Khosravi, executed In Iran For bilking money then buying Iranian property for Agenda 21

Another Banker Dead: IRAN Executes Rothschild Billionaire On $2.6 Billion Bank Fraud ~ Used Fraudulent Funds To Implement Agenda 21 In Buying State Property.

Here readers need to understand the consequence of allowing banks to lend what they do not even possess. A simple, hypothetical example will illustrate the principal-of-insanity which is the basis of our current monetary system .

Suppose JPMorgan holds $1 billion in total deposits. In the original form of our fractional-reserve fraud, the fraud ratio was set at 10:1. This meant that for every dollar which a bank actually held, it was allowed to “lend” $10. Now the simple arithmetic.

JPMorgan is holding $1 billion of other peoples’ property, but it is allowed to “lend” a total of $10 billion. Where does the other $9 billion come from? It is literally conjured out of thin air , via fractional-reserve fraud.

Thus, for many readers, this represents their first, actual glimpse of the full fraud, and full insanity of our current monetary system.

In the original form of our “fractional-reserve” monetary system, for every $1 which our central banks officially printed, the banking system created an additional $9 out of thin air, via fractional-reserve fraud. Simply put; 90% of all the actual “money” in our monetary system, and our economies, was conjured out of thin air , by private banks, via fractional-reserve fraud.

-

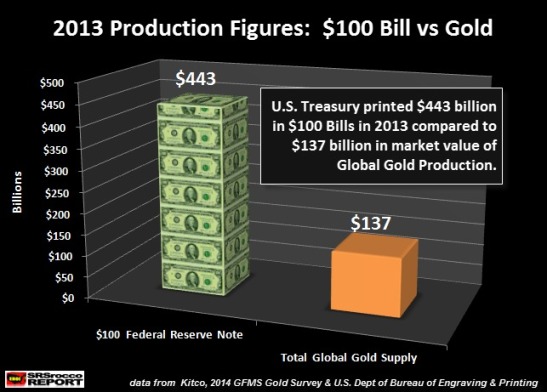

Precious Metals Are An Insurance Against The Failure Of The Fiat aka; ‘Counterfeit’ Federal Reserve Note, aka The “Dollar.”

-

Globalist’s Federal Reserve ~ The Dollar’s Homecoming: Gold & Silver Shorting By Bullion Banks To Bolster Image Of Fiat U.S. Dollar.

This is fractional-reserve banking, presented as the naked fraud that it is: bankers “lending” not only more than what they possess, but lending out “money” which grossly exceeds the amount of capital in existence. Conjuring oceans of paper out of thin air. It is inherently criminal. It is inherently fraudulent.

-

China Escalates Crackdown On Corrupt Banking: 370 People Arrested In Illegal Foreign-Exchanges Totaling $64 Billion.

-

China & Russia Protecting Physical Supply & Demand Of Capitalism: Keynesianism’s Paper Derivative Ponzi Scheme Imploding!

It automatically transforms our monetary system into an institutionalized Ponzi-scheme.

By definition, all “fractional-reserve banking systems” must automatically collapse – in a sea of fraud – if all depositors simply claim a tiny portion of their deposits, at any one time.

This is also known euphemistically as a “run on a bank”.

-

US Banks Told To Be Prepared For 30-day Crisis ~ Rothschild’s Last Stand!

-

Central Bankers & US Government Now Preparing For Dodd Frank Basel III Bail-Ins.

-

McCain’s Deadlier Version Of NDAA Passed By Belligerent Senate In Preparation For Reset.

-

April 2016 Sends A Soaring 562,000 Americans Missing From Obama’s Employment Calculations: The Final Silver & Gold Showdown!

Here, however, the euphemism is intended to insinuate that the mere act of depositors taking possession of their own property is somehow a “crime” against that financial system. Indeed, directly implying as much, our own governments will institute “bank holidays”.

This is yet another banking euphemism where depositors are legally prohibited from taking possession of their own property. The most recent example of such financial oppression was in Greece .

-

Greece Receives 1000 Bitcoin ATMs.

-

Syria: U.S. & Israeli ISIS Mercenaries Decimated by Iraqi, SAA, Kurd, and Russian Forces.

How can governments justify such financial oppression? While it is never explicitly acknowledged, the justification is entirely singular: to prop-up a Ponzi-scheme. It thus becomes necessary for governments to abandon the Rule of Law, and legally prevent/prohibit their own citizens from taking possession of their own property – as the only means of preventing the complete implosion of that system. The epitome of a Ponzi-scheme.

Observe how totally perverted and totally criminalized is the current system of fractional-reserve fraud. The banks are legally allowed to commit the crime of conversion: “lending” what they do not own.

The banks are legally allowed to commit fraud: “lending” what does not even exist. But if/when Depositors seek to take possession of their own property; they are treated like criminals.

The bankers are granted absolute legal protection to perpetrate their fraud/crime, at the direct expense of the law-abiding citizens of that society.

-

Iceland Sends 26 Corrupt Bankers To Prison.

-

Iceland Follows President Jefferson’s Warning About Debt Load.

-

Every Icelander To Get Paid In Bank Sale: 26 Bankers Behind Bars!

However, this marks only the starting-point for our present system of monetary/financial fraud. In its original form; fractional-reserve fraud was already entirely criminalized, and already entirely fraudulent. How/why would our governments have ever turned our entire financial system into such institutionalized fraud?

They were convinced to do so on the basis of the promise/guarantee of the bankers. The bankers promised that they would exercise the enormous, legal privilege which they had been granted by acting in a responsible manner, and doing nothing to jeopardize this institutionalized Ponzi-scheme.

In reality; the banks have done the precisely the opposite. First the Big Bank crime syndicate had their servants in our puppet-governments tear-up the legal distinction between “banking” (institutionalized fraud) and “investing” ( institutionalized gambling ).

Overnight, our banks were transformed into bank-casinos.

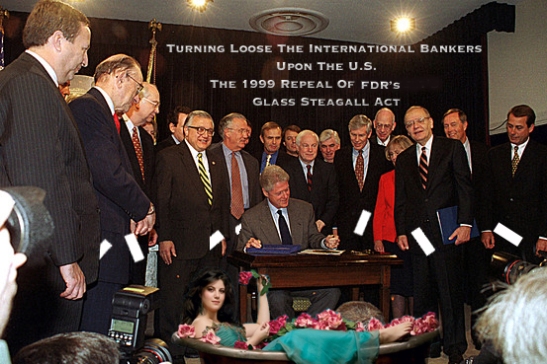

Clinton’s 1999 Green Light For Banks To Make High Risk Investments Against The Middle Class!

Billy Clinton Turned Loose The International Banks Upon The U.S. 1999

Not only were these “banks” lending-out funds which grossly exceeded their current assets, they were gambling with these funds, and at even greater ratios of leveraged fraud. The result of combining extreme fraud with extreme financial recklessness was the Crash of ’08.

The Big Banks literally “blew up” the Western financial system with their extreme, reckless gambling – gambling which began with the deposits which they claimed to be holding as trustees.

-

Deutsche Bank executive given four-and-a-half years for insider trading

-

It Begins ~ German Bank Charges Negative Interest As Economic Collapse Approaches: G20 Bloodsuckers Classify Your Savings As Paper Investments.

Instead of our governments punishing these Big Banks for their extreme, reckless fraud, they rewarded them. Using our money; these Traitor Governments indemnified the Big Banks for every cent of their reckless, fraudulent gambling. Then they did something much, much worse.

Our Traitor Governments bowed to the will of their banker Overlords, and dubbed these institutions of fraud/crime as being “too big to fail”. Translation? Instead of preventing these institutions of financial crime from continuing their reckless gambling, they promised to pay-off all of the banksters’ gambling debts, forever.

What happens when you tell any Compulsive Gambler that you will make-good on all of their gambling losses?

The Gambler runs wild. Observe what the banking crime syndicate calls “the derivatives market”.

Majority Sunni Minority Shiite

It is their own private, rigged casino, where the total amount of ultra-leveraged betting is twenty times as large as the entire global economy .

-

Russia Blasts The U.S. ~ For Dividing Iraq By Cabal’s Zionist Design Since 2006!

-

Egypt’s Grand Mufti Upholds Muslim Brotherhood’s Ex-President Morsi Death Sentence.

-

Mortal Enemy Of Iraq Is The U.S.’s IMF ~ Iraq Authorizes Russian Airstrikes Against ISIS: Iraqi Forces Seize U.S. Military Hardware From ISIS

-

Iraqi Government Signs $1 Billion Military Agreement With Russian Government: Providing Heavy Artillery, Ballistic Missile Systems And Ammunition.

It gets worse when the interest on ‘loans’ gets factored in.

Interest on IMF loans never gets paid off usually, the countries in the Third World being purposely kept in poverty so they can only ever pay interest back on the ‘loans’, and not the initial loan amount itself on top of the interest, keeping them as perpetual debt slaves.

Banks lend you £100,000 to buy a house, of which only £10,000 is real money, as they print the other £90,000 from thin air.

The person that you buy the house from then helps create massive inflation by spending this money.

Over 25 years, you must repay this money, totalling around £300,000 now with interest, SO YOU PAY BACK 30 TIMES WHAT YOU REALLY BORROWED.

And all the inflation is produced by this type of scam.

And where did the vast majority of that original £10,000 come from in the first place, on which the banks based their mortgage ‘loan’ scam? From the same fraud of course.

SOLUTION:

Non-Usurious banking, with all savings of the nation coming from real commodities and real labour put into a national pool, from which all society can draw from as a public service with zero interest repayable on loans, and zero charges either, and just as we draw books at no charge from a library, with the librarians being paid from public funds, so the wages of the bankers, with now very different roles, no more gambling on the stock exchange etc., with their wages now being more reasonable, and no more ridiculous ‘bonuses’, can also have their wages paid from public funds, just like any other public servant, just like a road sweeper for instance, who has his wages paid from public funds also.

That is as complex as it needs to get, we don’t need convoluted fancy alternative economic ‘systems’ dreamt up by whiz kids, this is it, this is the system that National Socialist Germany used, pure simplicity, perfect, with no goods being sent to other countries in exchange for useless paper money, which could then become massively devalued before it got spent by Germany, so only solid commodities from one country were exchanged for solid commodities from another country without the slightest possibility of fraud being able to enter the equation.

We could all have our houses paid for in 2 or 3 years on average maximum, and much bigger houses at that, and grow much if not all of our own food in massive gardens that would come with them, houses then being vastly cheaper.

BUT the pigs do not want this to happen, as we could largely secede from their scheme of things and retire almost, or just work 8 or 10 hours a week maximum to sustain ourselves very comfortably, much more comfortably than now, so the banks dangle the mortgage carrot in front of our noses all the best years of our lives, keeping us working almost literally for nothing, the essential product for them being our total exhaustion, mental, physical and spiritual, and they simply burn the money off on endless wars, ‘blowing stuff up’ for kicks, then getting the robotic goyim to build it all back up again. All this maintains the desired subjugation of the Gentiles by the Jews over us.

The Jews are scared that if they do not screw us down like this, we will have so much freedom and time on our hands that we might actually become more intellectual and wise to their criminal chicanery and terrorism.

The most essential purpose of our lives in this world is to learn to progress beyond this world, back to our original dimension of spiritual existence. The Jew has no intention of permitting us to accomplish this and escape from under their draconian rule, as we can be used here as slaves to make their lives ones of luxury and power.

If we are allowed to have more time to devote to spiritual culture, as well as the arts etc., then they will lose their grip over us, and the Jewish rabbinical opinion is nothing less than this; that if any people sees itself as equal to the Jews, as being naturally entitled to certain freedoms that the Jews enjoy, then that is to be taken as an act of PHYSICAL AGGRESSION against the Jews, which MUST BE MET BY PHYSICAL WARFARE AGAINST THAT PEOPLE.

Such a fate was experienced by Germany, so any attempt to free ourselves from the grip of the Jews in the future must be made by a huge federation of countries, much too big for the Jews and their NATO to take down.

Reblogged this on Mothman777's Blog.

That main picture has nothing to do with fractional-reserve banking and misrepresents bank transactions. In theory, the bank has to maintain a ratio range of what “money” it creates vs that it has reserved – said to be about 10 to 1. Any person’s deposited money into the bank results in the bank’s liability to that person for the amount deposited. And the bank has to keep to around a 10 to 1 reserves ratio based on that money. But that bank does not technically lend THAT money out again. Its lending is based on its reserves. If you were to withdraw that money, then the bank would have to arrange things to accord with its reserves policy (recover the 10 times it might have created based on that).

If one wanted to look at it in the simplified way as that picture: the $1000 gets deposited in the bank. The bank then owns that $1000 and the depositor has a $1000 banknote. The bank MAY end up lending out $10,000 based on that $1000 deposit. It DOES NOT lend $900 of a $1000 deposit, it “creates” up to $9000 based on a $1000 deposit. But none of that $9000 is from the $1000 deposit. If the depositor were to call in the $1000 banknote from the bank, the bank would have to make sure it still met its reserve requirements.

So generally speaking, the bank “creates” money. That “money” is obligations to pay bank loans. The bank can make loans based on reserve requirements (and a few other things not pertinent). In a way then, “money” is just “financial activity with a bank” (the “money” we are talking about here … let’s keep this simple). But if depositors call in banknotes, the bank has to arrange to not fall outside reserve requirements.

The picture has NOTHING AT ALL to do with what I just explained (fractional reserve banking).

This short clip may explain fractional reserve banking briefly.

mothman777 explained it very well.

https://youtu.be/FuHQhGqZvY0

I just read mothman777’s comment where he mentions this idea of “real money”. The bank’s note is “real money”. And it is the “real money” we use in the manner it is. I personally don’t care for this current system; but there is nothing not “real” about the bank’s money that it creates in its loans according to the rules it has to follow. When you use its money, you are obliged to play by its rules. There’s nothing not “real” about that.

If you so chose you could use anything as “money” between yourself and whomever you trade with. If you agree to use the default “money” (Federal Reserve based bank money) and pay interest for 30 years, that is up to you. You could prefer some other method of buying the house. You, and most people, don’t get the point that this system is “real money” every bit as much as your sitting on a pile of gold or something. Your obligation to pay their loans is “real money”, just as you owe the seller of a house an alternate agreed upon “real money” if the seller wishes for you to pay for the house in some non-interest-bearing way. The agreement to pay a loan is a perfectly sensible basis for money – particularly for people without hard assets.

@blake121666

I take it that you work for the banking system with all the bullshit you spout here. Why don’t you take it somewhere else?

@mothman777

The previous contender to the current bank system of loans of bank money and that “money” being “your obligation to pay it” was to be a chattel slave or indentured servitude or such type things for people not sitting on a pile of gold. Or I suppose you could be a brigand or marauder or something? If you’re going to bitch about the banking system, you should at least have a proper perspective.

What you called your “solution” above is communistic. How does the market decide the “worth” of goods and services in your system? It doesn’t, bureaucrats do. What you keep referring to as “real” is bureaucratically defined in your utopian “solution”. That is not “real” by any means.

The IMF you mention is off-topic.

The system I described is not Communistic, but National Socialist.

That is a nationalist system, that can also be used in international trade, even for limited trade with capitalist countries where those countries agree to trade in solid commodities for a particular trade, rather than in paper.

That system, as you well know, was very successfully practiced in Germany, so people are not all animals like you seem to think.

A federation of independent nations, each with compatible non-usurious means of trading would be ideal.

It takes people not obsessed with screwing each other over to participate in it, but you cannot conceive that such people could ever exist, or rather, you do not want to discuss the possibility of such people being able to exist, to keep the mental perspective of everyone on a moronic level.

The banks need that limited perspective to be maintained, to stop people having the trust to lend to each other without charge, without interest.

When people can be made to believe that others are naturally evil and all out to exploit them, then the alternative highly ordered exploitative system that criminal banking provides seems a positively benevolent thing in comparison to the bogey man of unlimited robbery, enslavement and loan-sharking that mankind will supposedly engage in otherwise. BUT REALLY, USURIOUS BANKING IS THE ULTIMATE BOGEY MAN.

“IF MY SONS DID NOT WANT WARS, THERE WOULD BE NONE”. SPOKEN BY GUTLE SCHNAPER, WIFE OF MAYER AMSCHEL ROTHSCHILD.

You’ve gotten way off the subject of fractional reserve banking – which Germany used under the NSDAP. Germany had been probably the most well-educated population in the world for many decades when the NSDAP came to power and lead the world in very very many fields of endeavor. The NSDAP implemented a large number of social projects and were very family friendly in some of its economic policies. But they actually never did get around to implementing any of Feder’s anti-usury ideas. Germany used fractional reserve banking like all other western countries did at the time. There is ALOT of bad information out there which I am afraid you have naively believed. You have been duped by communistic deceivers who favor command economies and want you to believe that Germany implemented some of their very bad ideas. Germany did not do that at all.

https://realcurrencies.wordpress.com/2013/09/16/hitlers-finances-and-the-myth-of-nazi-anti-usury-activism/

This is my last post. We have gone way off topic. You have been propagandized to believe untrue things.

I only posted initially to point out the error in the cartoon and explain fractional reserve banking in a more logical non-biased way than this article does. There is no fundamental fraud going on with fractional reserve banking as this article contends. Although there probably IS fraud in there somewhere – it isn’t at the fundamental level this article is saying. And the cartoon is just a pointless cartoon of course. When you have a productive endeavor that a bank is willing to loan you money for in return for your promise to pay that loan, that is all legitimate “bank money” that everyone accepts as legal tender. You have created money into the bank money system with your loan and you and the bank need to follow rules for this “money”. There is no fundamental fraud of the bank selling you something it does not have. The bank has the ability to create money into the economy in this way in keeping with the rules governing that. No fundamental illegality in any of the basics. There very well could be in the governing rules and laws though.

Fractional reserve banking doesn’t HAVE to imply usury, you know? There are models of zero and negative interest loans out there. You might want to hone your understanding of these things – try to stay away from the erroneous “Nazis did away with usury” BS.

You write with the air of authority, yet the article link https://realcurrencies.wordpress.com/2013/09/16/hitlers-finances-and-the-myth-of-nazi-anti-usury-activism/ that you provided to substantiate your assertions is itself not well thought out, containing such gems of non-logic as the following;

“Schacht’s and Hitler’s policies allowed full control of the economy, which was used to maximize production for the sake of war.”

“In fact, after the Nazi economy began to boom due to heavy spending on rearmament, it seems interest rates were raised to combat inflation.”

These two quotes above would seem to be contradicted by the following, that demonstrate that Hitler was not actually intending or seriously preparing for war. He was certainly not preparing to attempt to take over the world as the maniac Allied propaganda asserted. Hitler had in fact offered to destroy every weapon that the German armed forces possessed if the nations surrounding Germany were willing to do the same, but none were.

Germany only entered Poland very reluctantly after 58,000 German civilians forced to live in Poland in German territory that had been ceded to Poland after the post WWI Treaty of Versailles were brutally slaughtered by Jewish-led gangs of terrorists, in the same manner as the Jewish-led terrorist gangs of the 1917 Russian Red Revolution. Hitler’s pleas for peace to Poland were repeatedly ignored by the Polish government, and Germany was suckered into entering Poland just so war could be declared on her by previous arrangement.

See also;

https://pridecomethbeforeafall.wordpress.com/2014/02/10/hitlers-economic-miracle/

“Poland wants war with Germany and Germany will not be able to avoid it, even if it wants to.”

– Rydz-Smigly, Chief inspector of the Polish army in a public speech in front of Polish officers (Summer 1939)

“It will be the Polish army that will invade Germany on the first day of war.”

– The Polish ambassador in Paris (15.8.1939)

“Hitler and the German people didn’t want this war. We didn’t answer Hitler’s various petitions for peace. Now we have to admit that he was right. Instead of a cooperation with Germany, which he had offered us, now stands the gigantic, imperialistic might of the Sovjets. I feel ashamed to see how the same intentions which we accused Hitler of now are pursued under a different name.”

– Sir Hartley Shawcross, British chief-accuser in Nuerenberg

“We made a monster, a devil out of Hitler. Therefore we couldn’t disavow it after the war. After all, we mobilized the masses against the devil himself. So we were forced to play our part in this diabolic scenario after the war. In no way we could have pointed out to our people that the war only was an economic preventive measure.”

– US foreign minister Baker (1992)

HOW WOULD THE ECONOMY BOOM IF MUCH OF THE GNP OF THE POVERTY STRICKEN GERMANY WAS FRITTERED AWAY ON ARMAMENTS?

The eminent historian AJP Taylor has stated that Germany was not prepared for world war, nor preparing for it. You cannot borrow paper from a foreign Jewish bank, buy arms with it, and then pay that paper money back, with interest, having spent what was allegedly borrowed on a non-productive thing, armaments, and then see a growth in the economy or an improvement in the general standard of living.

Hitler’s Germany had it’s own steel production facilities to make it’s own arms around the cities along the Ruhr Valley, which contains huge coal and iron ore fields, Germany did not have to buy materials from abroad with borrowed paper to make any arms either, as the materials were present on German soil, and all that was required was German labour to use those resources.

If paper money had really been borrowed by Germany from foreign Jewish banks under usurious agreement, to pay those German workers, then more work would then have then to be done by German workers to pay that borrowed money back, with interest, and how would that improve the German economy? Of course, such a policy would actually impoverish the German economy still further.

And surely, if Germany had still been engaging in borrowing money under usurious agreement, to pay for non-productive goods, things that would simply be blown up in wartime, then how could the economy improve, of course it could not, yet it did, so the idea that Germany borrowed money Jewish from banks and thus improved it’s economy cannot be correct.

If Germany had simply been borrowing to buy goods, especially commodities for war, then the Weimar conditions of mass inflation would simply have returned, but the opposite occurred instead, indicating that whatever Hitler really did, it was not based on the same economic strategy as the earlier usurious Weimar economic model.